ECONOMICS PAPER 2 GRADE 12 MEMORANDUM - NSC PAST PAPERS AND MEMOS JUNE 2016

Share via Whatsapp Join our WhatsApp Group Join our Telegram GroupECONOMICS P2

GRADE 12

JUNE 2016

NATIONAL SENIOR CERTIFICATE

MEMORANDUM

SECTION A (COMPULSORY)

QUESTION 1

1.1 MULTIPLE-CHOICE QUESTIONS

1.1.1 C ✓✓ A maize manufacturer in the Eastern Cape

1.1.2 A ✓✓competition.

1.1.3 A ✓✓ monopoly

1.1.4 B ✓✓ more price elastic

1.1.5 B ✓✓ unskilled

1.1.6 B ✓✓ price war

1.1.7 C ✓✓ Physical capital cannot be reallocated easily.

1.1.8 A ✓✓encourage producers to supply important essential goods

(8 x 2)

(16)

1.2 MATCHING ITEMS

1.2.1 E ✓ All factors of production are variable

1.2.2 H ✓ quantity demanded is exactly equal to the quantity offered at a given price

1.2.3 B ✓ Contributes to increased competition in some markets, especially in retail trade

1.2.4 G ✓ The marginal revenue curve runs below the demand curve

1.2.5 I ✓ Can be easily replaced

1.2.6 A ✓ Quantity supplied drops

1.2.7 C ✓ One firm fixes the price and other accept it as a market price

1.2.8 F ✓ Funded by taxes (8 x 1)

(8)

1.3 CONCEPTS

1.3.1 Market ✓

1.3.2 Price discrimination ✓

1.3.3 Patent ✓

1.3.4 Oligopoly ✓

1.3.5 Total revenue ✓

1.3.6 Black market ✓

(6)

TOTAL SECTION A: 30

SECTION B

QUESTION 2

2.1

2.1.1

- Net present value (NPV) ✓

- Internal rate of return (IRR) ✓

- Cost benefit ratio (CBR) ✓

(2)

2.1.2

- It serves as a frame of reference or a standard when comparing markets ✓✓

- It is a good point of departure for any analysis of the way prices and production are determined in practice ✓✓

Accept any relevant explanation (Any 1 x 2)

(2)

2.2

2.2.1

- It is used to describe inefficiencies/efficiencies ✓✓

- Shows productive and allocative inefficiencies/efficiencies ✓✓

(Any 1 x 2)

(2)

2.2.2

- Indifference curve ✓ (1)

- Allocative and productive inefficiency/some resources are not used ✓ (1)

- Production possibility curve ✓ (1)

2.2.3

- Both B and C indicate productive/technical efficiency since they are on the PPC✓✓

- Although both points show productive efficiency only point C shows allocative efficiency ✓✓

- At point C the indifference curve is tangent to the PPC ✓✓

- It is only at point C that the consumers’ desires are met - the desired combination of goods is produced ✓✓ (Max 5)

(5)

2.3

2.3.1 Transport ✓ (1)

2.3.2 Artificial ✓ (1)

2.3.3

Natural monopoly

- High development costs prevent others from entering the market and therefore the government supplies the product ✓✓ (1 x 2)

Artificial monopoly - The barriers of entry are not economic in nature, for example, patent, licensing, create monopolies ✓✓

Accept any relevant differentiation (Any 1 x 2)

(4)

2.3.4

- Consumers are often exploited because a monopoly is the only supplier of a product ✓✓

- A monopoly does not produce at the minimum point of the long term average cost curve and produces few quantities but demands higher prices ✓✓

- Therefore consumers have to pay high prices for few goods ✓✓

- Some consumers are excluded from the market because they are not willing or able to pay the higher price ✓✓

Accept any relevant explanation (Any 2 x 2)

(4)

2.4

- Non-price competition involves firms distinguishing their products from competing products on the basis of attributes other than price ✓✓

- Non-price competition involves promotional expenditures ✓✓

- Trying to improve quality and after sales servicing, such as offering extended guarantees ✓✓

- Spending on advertising, sponsorship and product placement ✓✓

- Sales promotion ✓✓

- Firms will engage in non-price competition, in spite of the additional costs involved, ✓✓

- because it is usually more profitable than selling for a lower price and avoids the risk of price wars ✓✓

- Expanding to new markets by diversifying the product range ✓✓

- Extending trading hours ✓✓

Free deliveries and installation ✓✓ (Any 4 x 2)

(8)

2.5

- Entry into the market is easy ✓✓

- The economic profit the business made in the short term attracts new businesses to enter the market ✓✓

- The entry of new firms leads to an increase in the supply of differentiated products ✓✓

- Competition causes all economic profit to disappear, which means that long-term average cost equals the price of the product ✓✓

- The excess profits are eliminated in the long run through imperfect emulation of successful product design, production systems, and marketing efforts by both established and new competitors ✓✓

- Only normal profit is made in the long run ✓✓ (Any 4 x 2)

(8)

[40]

QUESTION 3

3.1

3.1.1

- There is only one seller of the product ✓

- There are barriers to entry/entry is blocked ✓

- The monopolist is regarded as a price maker✓

- There are no close substitutes ✓

- There is no competition ✓

- Products are unique ✓

- They may enjoy favourable conditions ✓

- They decide on production levels ✓

- They are faced with demand curves ✓

- They may exploit consumers ✓

- Large amounts of starting capital are required ✓

- It is also possible for the monopolist to make an economic profit in the long run ✓ (Any 2 x 1)

(2)

3.1.2 Economic costs include explicit and implicit costs while accounting costs only take into account explicit costs only ✓✓ (2)

3.2

3.2.1 Imperfect market ✓ (1)

3.2.2 Quantity 5 ✓✓ (2)

The reason is that TR=TC ✓✓/it is where profit is zero ✓✓

(Any 1 x 2)(2)

(4)

3.2.3

- = 12 ✓

- = 32 ✓

- = 15 ✓

- = 6,5✓

- = -15 ✓

(5)

3.3

3.3.1 Monopolistic market ✓ (1)

3.3.2 large number of producers ✓ (1)

3.3.3

- Products are not identical ✓✓

- Clothes are similar in many ways but are not totally identical ✓✓

- The similarity lies in the fact that they satisfy the same consumer need ✓✓

- The difference is that they differ in quality and style ✓✓

(Any 2 x 2)

(4)

3.3.4

- The equilibrium price of a monopolistic is higher than that of a perfect competitor ✓✓

- The monopolistic competitor does not produce at the minimum of the LAC whereas the perfect competitor does ✓✓

- The perfect competitor produces more at a lower price while the monopolistic competitor produces less at a higher price ✓✓

(Any 2 x 2)

(4)

3.4

- CBA helps to make better decisions on how scarce resources are allocated to satisfy wants ✓✓

- Thus a project that maximizes benefits compared to costs should be chosen ✓✓

- Decisions by people, businesses and governments are important for the society – involves allocation of scarce resources ✓✓

- It also provides us with deciding alternate solutions to specific problems ✓✓

- The feasibility of the project is determined by subtracting costs from benefits ✓✓ (Any 4 x 2)

(8)

3.5

Mark allocation

Max 4 marks (4) |

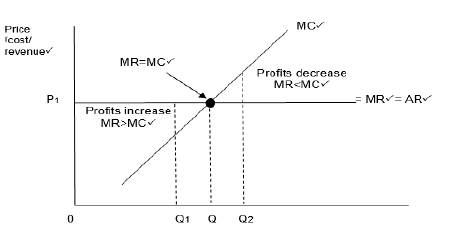

- The firm produces maximum profits if it produces the quantity where the marginal revenue is equal to marginal cost (MR=MC) ✓✓

- As long as marginal revenue is greater than marginal cost, the marginal revenue contributes towards total profits ✓✓

- By producing an additional unit, the producer gains the additional unit and his profit increases more than it cost to produce. MR>MC: profits increase ✓✓

- When the marginal revenue is less than marginal cost, total profits will decline ✓✓

- It costs the firm more to produce an additional unit than it gets from selling the additional unit it is therefore not in the interest of the firm to produce the extra unit ✓✓

- MR<MC: profits decline ✓✓

- If the marginal cost of producing an extra unit is higher than the marginal revenue received, the firm will make a loss ✓✓

- For the producer to maximise profits, it should expand production to the point where marginal revenue is equal to marginal cost ✓✓

(Any 2 x 2) (4)

(8)

[40]

QUESTION 4

4.1

4.1.1

- Cash grants ✓

- Interest free loans ✓

- Depreciation written off ✓

- Rent rebates✓

- Can be direct ✓ or indirect ✓

Accept any relevant example (Any 2 x 1)

(2)

4.1.2

- A supply curve is a phenomenon for price-takers and monopolists are price makers ✓✓

- Monopolies set the price at any quantity they choose to supply✓✓/they decide on production levels ✓✓

Accept any relevant explanation (Any 2 x 1)

(2)

4.2

4.2.1

- Marginal cost is the amount by which total cost increases when one extra product is produced ✓✓

Accept any relevant definition (Any 1 x 2)

(2)

4.2.2 Point S ✓✓ (2)

4.2.3

- A firm shuts down when it cannot meet its average or total variable costs ✓✓

- At point S the average revenue is less than average variable cost✓✓ (Any 1 x 2)

(2)

4.2.4

- The short-run supply curve of an individual producer is that part of the marginal cost curve that is above the minimum average variable cost ✓✓

- The supply curve starts from Point S upwards on the MC curve ✓✓

- At any point below the shut-down point the firm will not sell any goods ✓✓

- The firm will sell if the price is above the shut-down price level ✓✓

- If market price is rising as a result of an increase in market demand, this causes a shift in market prices ✓✓

- This means that quantity produced by the business increases as prices increase ✓✓

- The new equilibrium points plot the businesses supply curve at different market prices ✓✓ (Any 2 x 2)

(4)

4.3

4.3.1 Oligopoly ✓ (1)

4.3.2

- When there is a formal agreement between firms to collude it is called a cartel ✓✓

- A cartel is a group of producers whose goal is to form a collective monopoly in order to fix prices and limit supply and competition ✓✓

Accept any relevant definition (Any 2 x 1)

(2)

4.3.3

- Competition Commission ✓

- Competition Tribunal ✓

- Competition Appeal Court✓ (3 x 1)

(3)

4.3.4

- Reduction in output by firms/firms producing less ✓✓

- Consumers pay higher prices ✓✓

- Limited choice for the consumers✓✓

- Makes firms to inefficient ✓✓

- Lead to lack of innovation ✓✓ (Any 2 x 2)

(4)

4.4

- Transfers income directly to the poor e.g. child support grants, unemployment benefits etc. ✓✓

- Provides goods free of charge e.g. community goods, education etc. ✓✓

- Implements employment creation programmes e.g. public works programme ✓✓

- Subsidising merit goods e.g. subsidising arts and cultural events ✓✓

- Imposes taxes and laws on demerit goods to discourage consumption ✓✓

- Uses fiscal and monetary policy to achieve macroeconomic stability ✓✓

- Makes sure that consumers are informed about products through legislation ✓✓

- The South African Bureau of Standards (SABS) checks consumer goods in South Africa ✓✓

- Tries to prevent misleading advertising (Advertising Standards Authority) ✓✓ (Any 4 x 2)

(8)

4.5

KINKED DEMAND CURVE

Mark allocation

|

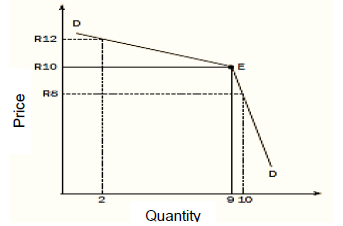

- The kinked demand curve model assumes that a business might face a dual demand curve for its product based on the likely reactions of other firms to a change in its price or another variable ✓✓

- The assumption is that firms in an oligopoly are looking to protect and maintain their market share and that rival firms are unlikely to match another's price increase but may match a price fall ✓✓

- That is rival firms within an oligopoly react asymmetrically to a change in the price of another firm ✓✓

- Suppose the oligopolist is selling at the original/present price of R10 and 9 units of output are sold. Total revenue is R10 × 9 = R90 ✓✓

- If the firm tries to increase profit by increasing the price by R2 to R12, quantity demanded would fall to 2 units and total revenue would decrease to R24 (R12 x 2) ✓✓

- If the firm tries to increase profit by reducing the price by R2 to R8 and increasing its total sales, total revenue would be R80 ✓✓

- The oligopolist is therefore faced with a difficult decision because in both instances it will not benefit ✓✓

- Increasing the price of goods or reducing the price to increase sales may not lead to greater revenue earned. The business would then lose market share and expect to see a fall in its total revenue ✓✓

- Due to interdependence within firms, a firm under oligopoly faces demand a kinked demand curve ✓✓ (Any 2 x 2) (4)

(8)

[40]

TOTAL SECTION B: 80

SECTION C

| STRUCTURE OF THE ESSAY | MARK ALLOCATION |

Introduction

| Max. 2 |

| Body Main part: Discuss in detail/In-depth discussion/Examine/Critically discuss/ Analyse/Compare/Evaluate/Distinguish/Explain/Assess/Debate. Max. 26 Additional part: Give own opinion/Critically discuss/Evaluate/Critically evaluate/Draw a graph and explain/Use the graph given and explain/Complete the given graph/Calculate/Deduce/Compare/ Explain/Distinguish/Interpret/Briefly debate | Max. 10 |

Conclusion

| Max. 2 |

| TOTAL | 40 |

QUESTION 5

Markets are broadly categorised into perfect and imperfect markets. However, in reality very few examples of perfect markets exist.

- Examine the conditions for the existence of a perfect market in detail.

(26) - Illustrate by means of graphs the position of the industry and firm in the long term if a loss was incurred in the short term.

(10)

[40]

INTRODUCTION

It is a market structure with a large number of participants who are price-takers. ✓✓The price is determined by the market demand and supply, This market is most efficient in the allocation of resources ✓✓

BODY

Characteristics:

- Products must be homogenous (i.e. identical) ✓

- Products must be identical. There should be no differences in style, design and quality. ✓✓

- In this way products compete solely on the basis of price and can be purchased anywhere. ✓✓

- There should be a large number of buyers and sellers ✓

- It should not be possible for one buyer or seller to influence the price. ✓✓

- When there are many sellers the share of each seller to the market is so small that the seller cannot influence the price. ✓✓

- Sellers are price-takers, they accept the prevailing market price. ✓✓

- No preferential treatment/discrimination ✓

- Buyers and sellers base their actions solely on price, homogenous product fetch the same price and therefore no preference is shown for buying from or selling to any particular person. ✓✓

- Free competition/Unregulated market ✓

- Buyers must be free to buy whatever they want from any firm and in any quantity. ✓✓

- Sellers must be free to sell what, how much and where they wish. ✓✓

- There should be no state interference and no price control. ✓✓

- Efficient transport and communication✓

- Efficient transport ensures that products are made available everywhere. ✓✓

- In this way changes in demand and supply in one part of the market will influence the price in the entire market. ✓✓

- Efficient communication keeps buyers and sellers informed about market conditions. ✓✓

- All participants must have perfect knowledge of market conditions ✓

- All buyers and sellers must be fully aware of what is happening in any part of the market. ✓✓

- Technology has increased competition as information is easily obtained via the Internet. ✓✓

- Freedom of entry/exit ✓

- There is complete freedom of entry and exit, that is to say the market is fully accessible. ✓✓

- Buyers and sellers are completely free to enter or to leave the market. ✓✓

- Mobility of factors of production ✓

- All factors of production are completely mobile, in other words labour, capital and all other factors of production can move freely from one market to another. ✓✓

- No collusion ✓

- In a perfectly competitive market, each buyer and seller acts independently from one another. ✓✓

NOTE: A maximum of 8 x 1 marks will be allocated for headings Max. 26

- In a perfectly competitive market, each buyer and seller acts independently from one another. ✓✓

ADDITIONAL PART

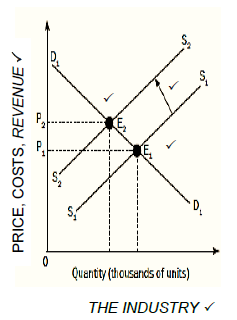

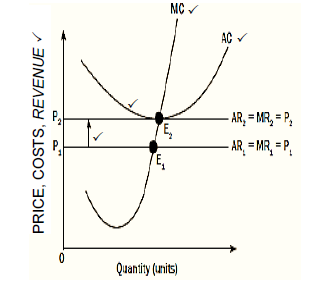

THE LONG TERM EQUILIBRIUM FOR THE INDUSTRY AND FIRM WHEN A LOSS WAS INCURRED IN THE SHORT RUN

MARK ALLOCATION:

MAXIMUM 5 MARKS FOR EACH GRAPH

(10)

CONCLUSION

The characteristics above indicate that the market has to meet strict requirements before it can be described as perfectly competitive. ✓✓ Although there are very few examples, the conditions of a perfect market does serve a frame of reference when studying other markets. ✓✓ (Accept any relevant conclusion)

(2)

[40]

QUESTION 6

Sometimes free market fail to produce the quantities of goods and services that people want at the prices that reflect marginal utilities and relative scarcities.

- Discuss the causes of market failure by referring to externalities and missing markets.

(26) - How does the government discourage or encourage externalities?

(10)

[40]

INTRODUCTION

A market failure is when the optimal production quantity is not produced and inefficiency occurs✓✓ Accept any relevant introduction n(2)

BODY

Externalities

- Externalities are costs not included in the pricing of goods/services, and consequently there is a difference between the private costs/benefits and the social costs/benefits of production. ✓✓

- Private costs are the cost of producing the good or service which translate into the prices that consumers pay. Also called internal costs. ✓✓

- Private benefits are internal benefits that accrue to those who produce goods and buy these goods, e.g. producing a bicycle (for producer) and using the bicycle (consumer). ✓✓

- Social costs are total costs incurred by society as a whole. ✓✓

- Social cost = private costs plus external costs. ✓✓

- Social benefits include the total benefit experienced by society as a whole. ✓✓

- Social benefits = private benefits plus external benefits. ✓✓

Negative externalities: - Are things like pollution, tobacco smoking and alcohol abuse. ✓

- The costs of negative externalities are paid by society rather than by the producers. ✓✓

Positive externalities - Are the positive effects of products to third parties which are not paid for. ✓✓

- Negative externalities are often over-produced while positive externalities are under-produced.

- This leads to market failure. ✓✓

Missing markets - Markets are incomplete because they cannot meet the demand for certain goods. ✓✓

Public goods ✓ - This includes community and collective goods and has two features:

- Non-rivalry: Consumption by one person does not reduce consumption by another individual, ✓✓ e.g. a lighthouse. ✓

- Non-excludability: Consumption can’t be confined to those who pay for it (free riders can use them), ✓✓e.g. radio and television ✓

- Social benefits outstrip private benefits ✓✓: e.g. health care and education. ✓

- Non-rejectability: Individuals are not able to abstain from consumption, e.g. street lighting.✓✓

- Continuous consumption. ✓✓E.g. traffic lights. ✓

Community goods ✓ - These are goods such as, defence, police services, prison services, streetlighting, flood control, storm water drainage and lighthouses. ✓

Collective goods ✓ - These are goods such as parks, beach facilities, streets. ✓

Merit goods ✓ - These are highly desirable for general welfare, but not highly rated by the market, e.g. health care, education and safety. ✓✓

- If people had to pay the market price for them, very little would be consumed. The market fails because the market produces less than the desired quantity. ✓✓

Demerit goods ✓ - These are over-consumed goods, e.g. cigarettes, alcohol and drugs.✓✓

NOTE: A maximum of 8 x 1 marks will be allocated for headings Any 26

(26)

ADDITIONAL PART

The government has used three methods to reduce negative externalities: ✓

- The government has carried out campaigns in order to change/persuade people from causing negative externalities. ✓✓

- Levying taxes on goods that cause negative externalities. E.g. Taxes are levied on cigarettes and alcohol. ✓✓

- Passing laws and regulations to prevent activities that cause negative externalities. ✓✓ E.g. Tobacco companies are not allowed to advertise. There are laws that regulate the amount of air pollution and waste. (5)

The government encourages positive externalities by: ✓

- Advertising on the radio or television. ✓✓

- Providing education, health care and other services at a low cost or free. ✓✓

- Providing consumer subsidies. ✓✓

- Consumer subsidies lower the cost of a good and encourage its usage. ✓✓(5)

Accept any relevant measure taken by the government

(10)

CONCLUSION

When market failures occur, it causes inefficiency and misallocation of resources and the government will have to intervene to recover the instability. ✓✓

Accept any relevant conclusion (2)

[40]

TOTAL SECTION C: 40

GRAND TOTAL: 150