ECONOMICS PAPER 2 GRADE 12 MEMORANDUM - 2018 JUNE EXAM PAST PAPERS AND MEMOS

Share via Whatsapp Join our WhatsApp Group Join our Telegram GroupECONOMICS PAPER 2

GRADE 12

NATIONAL SENIOR CERTIFICATE

MEMORANDUM

JUNE 2018

SECTION A (COMPULSORY)

QUESTION 1

1.1 MULTIPLE-CHOICE QUESTIONS

1.1.1 D ✓ individual businesses

1.1.2 A ✓ private

1.1.3 B ✓ average variable

1.1.4 D ✓ advertising

1.1.5 B ✓ discrimination

1.1.6 C ✓ quantity demanded is equal to quantity supplied

1.1.7 C ✓ marginal

1.1.8 A ✓ reduce (8 x 2) (16)

1.2 MATCHING ITEMS

1.2.1 E ✓ buyers and sellers do not have market power

1.2.2 G ✓ do not change as output change

1.2.3 A ✓ the holder is the only one who can produce the product

1.2.4 F ✓ cannot be recovered should the firm leave the industry

1.2.5 B ✓ makes super-normal profit in both the short and long term

1.2.6 I ✓ often exploited due to absence of ownership

1.2.7 C ✓ is an example of a negative externality

1.2.8 D ✓ Used in making the decision whether to accept/reject the project (8 x 1) (8)

1.3

1.3.1 Marginal product ✓

1.3.2 Maximum price ✓

1.3.3 Normal profit ✓

1.3.4 Positive externality/ external benefit ✓

1.3.5 Free rider ✓

1.3.6 Duopoly ✓ (6 x 1) (6)

TOTAL SECTION A: [30]

SECTION B

QUESTION 2

2.1

2.1.1 List any TWO examples of perfectly competitive markets

- Stock exchange ✓

- Foreign exchange markets ✓

- Agricultural sector ✓

(Accept any relevant example.) (2 x 1) (2)

2.1.2 How can the government use taxes to reduce production and consumption?

Taxes can be increased. ✓✓ (2)

2.2 Study the table below and answer the questions that follow.

REVENUE OF A MONOPOLY

| Quantity | Price | Total revenue | Marginal revenue | Average revenue |

| 1 | 50 | 50 | 50 | 50 |

| 2 | 40 | 80 | 30 | 40 |

| 3 | 30 | 90 | 10 | 30 |

2.2.1 How many sellers are in a monopoly?

One seller ✓ (1)

2.2.2 Which revenue is equal to the price?

Average revenue ✓ (1)

2.2.3 What is the formula for calculating marginal revenue?

Marginal revenue = Change in total revenue ✓

Change in quantity/units ✓ (2)

2.2.4 Briefly explain economies of scale as a barrier to entry in a monopoly.

New firms, with relatively low output, will find it difficult to compete because theirs average costs will be higher than the existing firms benefiting from lower average costs with increased output. ✓✓ (Accept any relevant correct explanation.) (2)

2.2.5 How are consumers affected by the existence of monopolies?

- Consumers are often exploited because a monopoly is the only supplier of a product ✓✓

- They have to pay high prices for few goods ✓✓

- Some consumers are excluded from the market because they are not willing or able to pay the higher price ✓✓

(Accept any relevant, correct explanation) (2 x 2) (4)

2.3 Read the information below and answer the questions that follow

UNIONS HAVE MIXED REACTION TO NATIONAL MINIMUM WAGE ANNOUNCEMENT.

|

2.3.1 Identify from the extract TWO groups of workers who are not included in this minimum wage agreement.

- Farm workers ✓

- Domestic workers ✓(2)

2.3.2 Briefly describe the concept minimum wage.

A wage rate set, above the equilibrium wage rate, by the government, below which no employer can pay their workers ✓✓ (2)

2.3.3 Explain the impact of a minimum wage on demand and supply of labour.

The demand for labour decreases while the supply increases. ✓✓ (2)

2.3.4 Why is the national minimum wage good for South Africa’s economy?

Minimum wage is good for South Africa because it can:

- Reduce the income inequalities and poverty ✓✓

- Stimulate economic growth ✓✓

- Lead to higher productivity by workers ✓✓

- Increase demand for goods and services because low income earners will have money to spend ✓✓

(Accept any relevant, correct response.) (2 x 2) (4)

2.4 Distinguish between a perfect market and a monopoly with regard to prices, profit, quantity and cost.

Prices

The monopolist produces at higher prices than the perfect competitor✓✓

Profit:

Under perfect competition, only normal profit will be made in the long term; ✓✓ the monopolist, on the other hand, can make economic profit in both the short and long term ✓✓

Quantity:

The monopolist produces less than the perfect competitor. ✓✓

Cost:

The monopolist does not produce at the lowest possible cost due to a lack of competition, ✓✓whilst the perfect competitor will always produce at the lowest possible cost due to competition. ✓✓ (4 x 2) (8)

2.5 How will new entrants in the perfect competitive market impact on the profit levels of existing businesses?

New entrants in perfect markets will impact on profit levels of existing businesses in that:

- New firms enter the market when existing businesses make economic profits in order to benefit from the profits ✓✓

- This increases the market supply. ✓✓

- the increase in supply leads to lower price levels of goods and services. ✓✓

- This causes smaller/lower profit than previously. ✓✓

- Production increases, until some businesses cannot cover their average variable cost any more ✓✓ causing the shut down and exit the market. ✓✓

- Only normal profits are realised in the long run. ✓✓ (4 x 2)

(Accept any correct, relevant answer.)

(Allocate a maximum of 2 marks for the mere listing of facts/examples.) (8)

[40]

QUESTION 3

3.1

3.1.1 List any TWO types of monopolies.

- Artificial monopoly ✓

- Natural monopoly ✓ (2)

3.1.2 What will the effect be if a firm in a perfect market decides to increase the price of its product?

Firm will make a loss, because all firms in the perfect market are price takers and cannot influence the market price. ✓✓ (2)

3.2 Study the information below and answer the questions that follow.

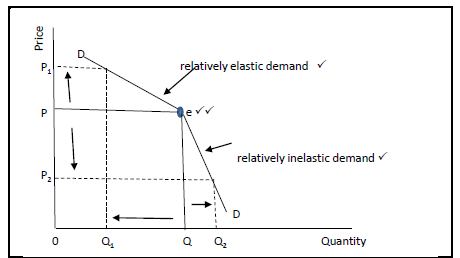

THE DEMAND CURVE OF AN OLIGOPOLISTIC FIRM The demand curve of an oligopolistic firm was developed in 1939 by the American economists Paul Sweezy. |

3.2.1 Who developed the theory on the demand curve of an oligopolistic firm?

Paul Sweezy ✓ (1)

3.2.2 What is the demand curve of an oligopolist firm called?

Kinked demand curve ✓ (1)

3.2.3 Briefly explain an inelastic demand.

Demand is not sensitive to a price change. ✓✓

A change in price causes a small change in demand. ✓✓ (1 x 2) (2)

3.2.4 Explain mutual dependence as a characteristic of oligopoly.

- One seller’s action will influence the other sellers ✓✓

- Each firm is aware of each other’s actions since the market is dominated by a few firms, e.g. cars. ✓✓ (1 x 2) (2)

3.2.5 Draw a fully labelled kinked demand curve, indicating the segments and equilibrium.

(4 x 1) (4)

3.3 Study the information below and answer the questions that follow.

JASCO GIVES UP ON CROSS FIRE ACQUISITION

|

3.3.1 Which authority did not allow the merger of Jasco and Cross Fire?

Competition Commission ✓ (1)

3.3.2 What was the reason for the denial of the merger?

The merger will prevent or lessen competition in the provision of active fire protection systems. ✓ (1)

3.3.3 Explain any other two objectives of Competition Policy other than those in the extract.

- To prevent monopolies and other powerful businesses from abusing their power ✓✓

- To stop firms from using restrictive practices like fixing prices,

- dividing markets etc. ✓✓

- Improve the efficiency in the market through legislation ✓✓

- Protect the consumer against unfair prices and inferior products for example through the Competition Act ✓✓

Do not accept ‘preventing mergers and acquisitions’ and ‘promoting healthy competition’. (2 x 2) (4)

3.3.4 In your opinion how will the economy benefit from fair competition?

The economy will benefit because fair competition will:

- Open up opportunities for more entrepreneurs to join in to businesses✓✓

- Create more job opportunities ✓✓

- Lead to higher standard of living ✓✓

- Contribute to lower prices ✓✓

- Contribute to better quality goods and services ✓✓

(Accept any other relevant response.) (2 x 2) (4)

3.4 Distinguish between the short and long term/run.

Short term/run

- The short run is the period of production where only the variable factors of production can change. ✓✓

- The time period is too short to enable the number of firms in the industry to change. ✓✓ (2 x 2)

Long term/run

- The long run is the period of production where all factors can change. ✓✓

- The time is long enough for variable and fixed factors to change. ✓✓

- It allows enough time for new firms to enter the industry and/or existing firms to exit. ✓✓ (2 x 2)(8)

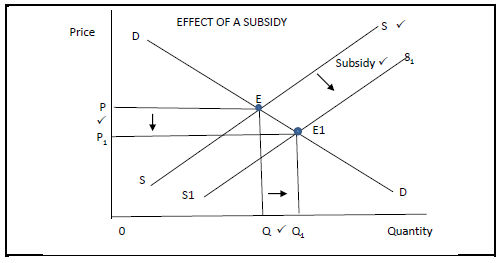

3.5 Explain, with the aid of a well-labelled graph, the effect of providing subsidies to producers as a form of government intervention during market failure.

Providing producer subsidies

- The government provides subsidies to producers in order to encourage them to increase the production of goods. ✓✓

- Supply increases from SS to S1S1 ✓✓

- Subsidies lower the cost of producing goods and thus the market price of these goods is lowered/decreased from 0P to 0P1 ✓✓

- The lower price allows people to buy more at Q1 ✓✓ (Max. 4) (8)

[40]

QUESTION 4

4.1

4.1.1 Give any TWO examples of community goods.

- Protective services ✓

- Street lights ✓

- Flood control ✓

(Accept any relevant, correct example.) (2 x 1) (2)

4.1.2 Why would consumers accept the existence of differentiated products as compared to homogeneous products?

Consumers like choices that result from product differentiation rather than to consume identical products that are produced by perfect markets. ✓✓

(Accept any relevant explanation.) (1 x 2) (2)

4.2 Study the information below and answer the questions that follow.

MONOPOLISTIC COMPETITION As long as consumers perceive the products to be different, then theyare different. |

4.2.1 Identify the market structure above.

Monopolistic competition ✓ (1)

4.2.2 Is the difference between the products above real or artificial?

The difference is artificial. ✓ (1)

4.2.3 Explain branding as a non-price strategy used by monopolistic competitors.

- Branding help firms in monopolistic competitive markets differentiate their products from those of their competitors. ✓✓

- Brands make it easy for the firm to advertise the product ✓✓

- Advertising can create brand loyalty in consumers. ✓✓ (Accept any other correct response.) (2 x 2) (4)

4.2.4 Why does monopolistic competition not have full control over the price?

- There are many sellers in the market. ✓✓

- Each business sells at its own price since a single price cannot be determined for the differentiated product because a range of prices could apply. ✓✓ (4)

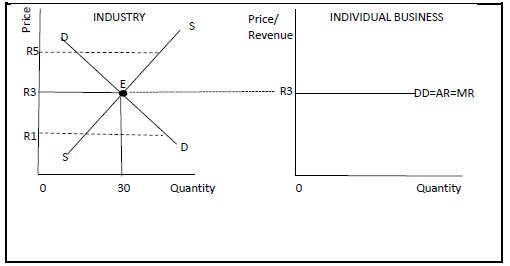

4.3 Study the graphs below and answer the questions that follow.

4.3.1 At which price will the individual business sell its products?

R3 ✓ (1)

4.3.2 How is the slope of the demand curve of the industry?

Negative slope ✓ (1)

4.3.3 Briefly explain the phrase businesses are price takers.

Businesses cannot determine their own price but take the price determined in the market. ✓✓ (2)

4.3.4 How are prices determined in the industry?

In the industry prices are determined by the intersection of demand and supply. ✓✓ (2)

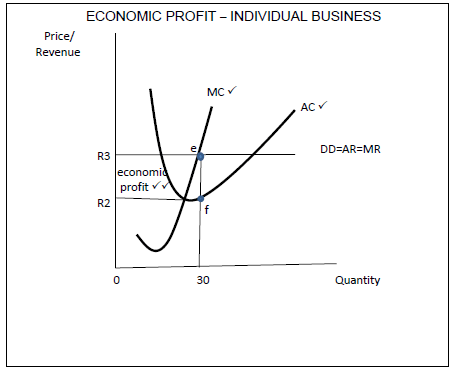

4.3.5 In your ANSWER BOOK redraw the graph of an individual business and insert curves that show the business making economic profit.

(4 x 1) (4)

4.4 Explain the uses of the cost-benefit analysis (CBA).

- The cost-benefit analyses is generally used in the public sector when evaluating large-scale public investment projects ✓✓ e.g. new highways, railway lines, airports, dams, ports and public transport. ✓

- The CBA is used to assess the net social benefit that will accrue to the population from these projects. ✓✓

- CBA requires careful definitions of the projects, accurate estimation of projects lives, and comprehensive consideration of externalities.

- Essentially, CBA concentrates on the economic efficiency benefits from a project. ✓✓

- The CBA can be used to redistribute income, by making payments to the losers and expect payment from the gainers through a levy or indirect

tax.✓✓ - The CBA is a tool/technique that seeks to bring greater objectivity to decision-making. ✓✓ (8)

4.5 Why will it not benefit a monopoly to increase its price excessively?

Increasing the price excessively will not benefit a monopoly because:

- Although the monopoly decides on production levels and determine their own prices, demand does not influence the price. ✓✓

- The monopoly is however influenced by the limited budget of consumers as they decide how much they will spend on a particular product. ✓✓

- Even though the monopoly is the only supplier of the product consumers may decide not to buy the product. ✓✓

- In as much as there are no close substitutes consumers may still substitute the product of a monopolist ✓✓ e.g. paraffin for electricity ✓

- Increasing the price too high will lead to lower revenue. ✓✓

(Accept any other relevant, correct response.) (8)

[40]

TOTAL SECTION B: 80

SECTION C

Answer any ONE of the two questions from this section in the ANSWER BOOK.

| STRUCTURE OF ESSAY | MARK ALLOCATION |

Introduction

| Max. 2 |

| Body Main part: Discuss in depth/In-depth discussion/Examine/ Critically discuss/Analyse/Compare/ Evaluate/Distinguish/ Explain/Assess/Debate | Max. 26 |

| Additional part: Give own opinion/Critically discuss/Evaluate/ Critically evaluate/Draw a graph and explain/Use the graph given and explain/Complete the given graph/ Calculate/Deduce/ Compare/Explain/Distinguish/Interpret/Briefly debate | Max. 10 |

Conclusion

| Max. 2 |

| TOTAL | 40 |

QUESTION 5: MICROECONOMICS

Examine in detail the oligopoly under the following headings:

- Nature of the product (6)

- Control over price (6)

- Collusion (14) (26 marks)

How can firms in an oligopoly increase their market share in the economy? (10 marks)

INTRODUCTION

An oligopoly is a market structure that has few large sellers that dominate the market. ✓✓

(Accept any correct relevant introduction.) (2)

BODY

Nature of the product

- Products sold may be homogenous or differentiated. ✓✓

- If products are homogeneous it is called a homogeneous oligopoly ✓✓– many industrial products are standardised for example steel products. ✓✓

- If products are differentiated it is a differentiated oligopoly ✓✓ – these firms produce goods such as household appliances, electronics equipment, breakfast cereals. ✓✓ (Max. 6)

Control over price

- Producers have considerable control over the price of their products, although not as much as in a monopoly. ✓✓

- Oligopolies can frequently change their prices in order to increase their market share. ✓✓

- This can result in a price war. ✓✓ (Max. 6)

Collusion

- Collusion takes place when rival firms cooperate by raising prices and by restricting production in order to maximise their profits. ✓✓

Cartel ✓

- When there is a formal agreement between firms to collude, it is called a cartel. ✓✓

- A cartel is a group of producers whose goal is to form a collective monopoly in order to fix prices and limit supply and competition. ✓✓

- In general, cartels are economically unstable because there is a great

incentive for members not to stick to the agreement, to cheat by cutting

prices, illegally and to sell more than the quotas set by the cartel. ✓✓ - Although there is an incentive to collude there is also an incentive to compete. ✓✓

- This has caused many cartels to be unsuccessful in the long term. ✓✓Some well-known cartels are the Organisation of Petroleum Exporting Countries

Overt/formal collusion ✓

- Overt/Formal collusion e.g. cartels are generally forbidden by law in most countries ✓✓

- However, they continue to exist nationally and internationally. ✓✓

Tacit collusion ✓

- Sometimes in an oligopoly market, a dominant firm will increase the price of a product in the hope that its rivals will see this as a signal to do the same ✓✓

- This is referred to as price leadership. ✓✓ (Max. 14)

(26)

ADDITIONAL PART

How can firms in an oligopoly increase their market share in the economy?

Oligopolies can increase their market share by using various strategies such as:

- Engaging in product differentiation, where the products are made to be slightly different in terms of physical appearance, packaging etc. ✓✓

- Improving after-sale-services that are far more important to customers and will ensure a long-term relationship with that business ✓✓

- Aggressive advertising to lure consumers onto their side ✓✓

- Establishing brand loyalty, because oligopolies want consumers to believe that its brand is the best and to buy only that brand ✓✓

- Engaging in product proliferation whereby oligopolies produce many different ranges of products to cater for many different markets ✓✓

- Extending shopping hours to encourage greater flexibility to households ✓✓

- Selling products online to make it easier for customers to shop around without any additional costs ✓✓ and a variety of goods is made available to make comparisons. ✓✓

- Paying loyalty rewards to customers for continued support. ✓✓

(Accept any other relevant, correct response.) (10)

CONCLUSION

Oligopolies can control the supply of the product or service on the market, in order to keep its prices and profits high. ✓✓

(Accept any other high order conclusion.) (2)

[40]

QUESTION 6

Discuss the following factors that lead to misallocation of resources in the market.

- Imperfect competition (8)

- Merit and demerit goods (10)

- Immobility of factors of production (8) (26 marks)

With the aid of well-labelled graphs explain productive inefficiency as a consequence of market failure. (10 marks)

INTRODUCTION

Market failure occurs when the forces of demand and supply fail to allocate resources efficiently. ✓✓

(Accept any relevant introduction.) (2)

BODY

Imperfect competition

- Competition in market economies is limited by the power of certain producers to prevent new businesses from entering the market. This is imperfect

competition. ✓✓ - Barriers to entry are created because of advertising, a lack of capital and the controlling of resources. ✓✓

- The imperfect market does not allow for price negotiations. ✓✓

- Advertising is used to promote producer sovereignty (dominance), which encourages consumers to buy existing products and allows producers to delay new products from entering the market until it is in their own interest ✓✓ (e.g. businesses have had the technology to produce long-life light bulbs for many years but have chosen not to launch them in the market). ✓✓ (8)

Merit and demerit goods

Merit goods:

- These are highly desirable for general welfare, but not highly rated by the market, e.g. health care, education and safety. ✓✓

- If people had to pay the market price for them, very little would be consumed. ✓✓

- The market fails because the market produces less than the desired quantity. ✓✓

Demerit goods:

- These are over-consumed goods, ✓✓ e.g. cigarettes, alcohol and drugs. ✓

- Thus more of the goods are produced than is socially desirable. ✓✓

- The government bans or reduces consumption of these products through taxation, and provides information to the population on their harmful effects. ✓✓ (Max. 10)

Immobility of factors of production

- Labour takes time to move from one area to another. ✓✓

- The supply of skilled labour cannot be increased because of the time it takes to be trained or educated. ✓✓

- Physical capital, like factory buildings or infrastructure such as telephone lines cannot be reallocated easily. ✓✓

- Structural changes like a change from producing plastic packets to paper packets or shifting from labour-intensive production to computer based production requires a change in labourers’ skills, employment and work patterns. ✓✓

- This takes time to change. ✓✓ (Max. 8)

(26)

NOTE: A maximum of 8 x 1 marks will be allocated for headings.

ADDITIONAL PART

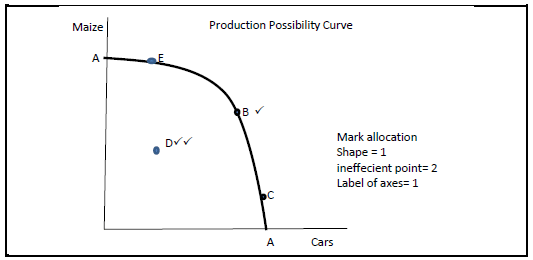

- Productive inefficiency can be explained with the aid of the productive possibility curve. ✓✓

- The Production Possibility Curve (AA), above shows a combination of goods that can be produced using all the available resources. ✓✓

- Any point on the curve shows a combination of goods where resources will be used efficiently. ✓✓

- Therefore any point on the curve indicates Productive/Technical efficiency ✓✓

- Any point to the left of the curve such as D, indicates that some resources are unused. If this occurs some customers may be deprived of goods. ✓✓

- This depicts productive inefficiency. ✓✓ (Max. 6)

CONCLUSION

When market failures occur, it causes inefficiency and misallocation of resources and the government will have to intervene to recover the instability. ✓✓✓

(Accept any relevant conclusion.) (2)

[40]

TOTAL SECTION C: 40

GRANDTOTAL: 150